How Does the Federal Solar Tax Credit Work?

The federal tax credit for homeowners buying solar panels outright ended on December 31, 2025, due to the One Big Beautiful Bill (OBBB). However, the commercial tax credit is still available.

The federal solar tax credit lowers a taxpayer’s federal tax bill by a set percentage of solar installation costs. The Internal Revenue Code splits this Investment Tax Credit (ITC) into 2 parts:

- Section 25D for homeowners

- Section 48E for businesses

The One Big Beautiful Bill Act, signed into law on July 4, 2025, ended Section 25D for new residential installations on December 31, 2025. Section 48E, however, still applies to commercial solar projects through 2027.

This change affects two distinct groups differently.

- Homeowners who installed systems before the residential deadline can still claim their credit on a 2025 tax return.

- Commercial investors, meanwhile, now face new construction deadlines and sourcing rules under Section 48E.

Continue reading to learn how the credit worked for homeowners, how it still operates for businesses, and exactly what the new law changed. We will also break down how to calculate your solar savings, which expenses qualify, and which state programs remain active in 2026.

Disclaimer: This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Consult a licensed tax professional for guidance specific to your situation.

What Was the Federal Solar Tax Credit?

The federal solar tax credit began under Section 25D, created by the Energy Policy Act of 2005, to encourage clean energy investment. The rate started at 30%, dropped briefly to 26% in 2020, then returned to 30% under the Inflation Reduction Act of 2022. That 2022 law extended the rate through 2032, before the One Big Beautiful Bill Act reversed the extension in 2025.

According to the Solar Energy Industries Association (SEIA), the U.S. solar industry grew more than 10,000% since the ITC’s 2006 enactment. Annual installations jumped from roughly 1 gigawatt in 2009 to nearly 50 gigawatts in 2024. That growth reflects the credit’s role in scaling both residential and commercial adoption, a pattern often cited in Inflation Reduction Act solar incentives research.

How a Tax Credit Differs From a Tax Deduction?

A tax credit cuts a tax bill directly, while a deduction only lowers taxable income before tax is calculated. This distinction sets the credit’s actual dollar value.

A $10,000 qualifying solar expense at the 30% ITC rate produces a $3,000 credit, reducing taxes owed by exactly $3,000. In contrast, a $10,000 deduction saves only about $2,200 for a taxpayer in the 22% bracket, since deductions reduce taxable income rather than the bill itself.

| Mechanism | Effect on Taxes |

| Tax credit (30% ITC) | Reduces tax owed directly |

| Tax deduction (22% bracket) | Reduces taxable income |

Here you can see why federal energy tax credits deliver more value than equivalent deductions for most taxpayers.

Federal Solar Tax Credit in 2026: What Changed?

The transition into 2026 marks a massive structural shift in how solar projects receive federal backing. With the OBBB Act fully in effect, the traditional path of buying residential panels to claim a personal credit is gone. The new landscape focuses strictly on commercial ownership. This means the 30% incentive hasn’t disappeared entirely; it has just migrated.

If you’re looking at solar for your roof today, your strategy has to shift. Instead of buying the system, look into companies that offer third-party options; they handle the backend business credits so you can still capture the savings indirectly. Partnering with a provider experienced in residential solar installation services allows you to navigate these lease options smoothly and benefit from reduced monthly utility costs.

Why is Roofsolar Still Valuable in 2026?

If you are thinking that Section 25D has completely eaten the residential solar, you need clarification. You know that hardware costs for solar panels and lithium-ion batteries have decreased, and traditional utility rates are increasing across the country.

Even without a direct federal tax write-off, investing in your own energy infrastructure pays for itself over time through long-term utility bill avoidance. You’re trading a volatile monthly electric bill for fixed, predictable energy independence.

About Active Commercial Solar Tax Credit (Section 48E)

Section 48E remains active for businesses, nonprofits, and third-party-owned residential systems through December 31, 2027. The credit starts at a 6% base rate and rises to 30% once a project meets prevailing wage and apprenticeship requirements.

Projects larger than 1.5 MW must now use the physical work test to prove a construction start date, since Treasury eliminated the 5% cost-based safe harbor for those systems under Notice 2025-42. Similarly, smaller systems of 1.5 MW or less can still use either method through July 4, 2026.

Section 48E terminates for facilities placed in service after December 31, 2027, unless construction began on or before July 4, 2026. FEOC rules, effective since January 2026, also restrict eligibility for systems sourcing key components from certain foreign-controlled suppliers. This commercial solar investment tax credit now demands earlier planning than before the law changed, making it critical to work with a team specialized in commercial solar installation services to lock in safe harbor status before deadlines expire.

The OBBB Depreciation Penalty

While Section 48E is still available for businesses, the OBBB Act introduced a significant financial adjustment. The law eliminated the favorable 5-year MACRS accelerated depreciation schedule for solar and energy storage facilities where construction began after December 31, 2024. If you are a commercial investor planning a project in 2026, you will need to evaluate your long-term ROI based on these updated depreciation timelines.

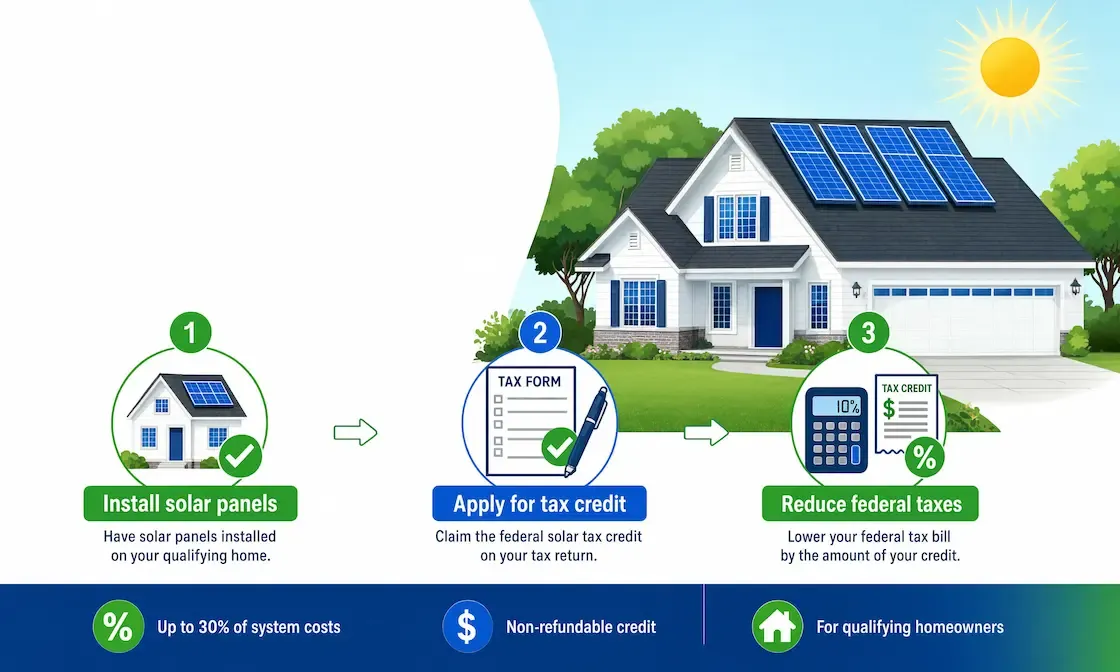

How Did the Federal Solar Tax Credit Work?

For homeowners who qualified before the cutoff, the credit worked by directly offsetting their year-end tax liability. Instead of acting as a point-of-sale discount, it required the homeowner to fund the project upfront through cash or a loan, track their total eligible expenses, and then apply that value to their federal tax return. This mechanism meant that the net cost of a solar project depended heavily on a homeowner’s personal tax appetite for that year.

Solar Tax Credit Calculation Formula

The formula multiplies total qualifying system costs by the applicable rate, as shown below:

Credit = System Costs × Credit Rate

Residential systems placed in service through 2025 used a flat 30% rate. See the table below for examples.

| System Cost | Credit Rate | Formula Implementation | Credit Value |

| $15,000 | 30% | =15,000 x 0.30 | $4,500 |

| $25,000 | 30% | =25,000 x 0.30 | $7,500 |

| $40,000 | 30% | =40,000 x 0.30 | $12,000 |

What Expenses Qualified?

Three expense categories qualified under Section 25D.

- Equipment costs covered solar panels, inverters, mounting hardware, and Energy Star-certified components.

- Balance-of-system costs covered wiring, labor, permitting fees, and sales tax on equipment.

- Storage costs covered batteries, but only systems with at least 3 kilowatt-hours of capacity, per IRS Form 5695 requirements.

For property owners who already have panels but want to expand their capabilities, utilizing specialized system add-on services ensures that newly integrated battery storage systems or retrofitted components meet these precise capacity guidelines to qualify for available credit structures.

What Expenses Did Not Qualify?

Standard roofing materials and structural roof repairs never qualified, even when reroofing was necessary before installation.

About Carryover Rules

Unused residential credit is carried forward indefinitely under Section 25D, since the statute never capped individual carry-forward years.

- A homeowner who owed less tax than their credit value in 2025 can apply the remainder in 2026 or later.

- Commercial Section 48E credits work differently: under IRC Section 39(a)(4), businesses can carry the credit back 3 years or forward up to 22 years. A business placing a system in service in 2026 could apply the credit against taxes owed anywhere from 2023 through 2048. This solar credit carry-forward strategy gives commercial filers far more flexibility than residential filers ever had.

Who Qualified?

The federal solar tax credit carried no income limit for eligible taxpayers, unlike some other federal energy credits. Eligibility instead depended on ownership structure and system type.

- Homeowners qualify by purchasing a residential system, whether through cash or a solar loan.

- Businesses qualify under Section 48E regardless of size, provided they own the system and meet construction deadlines.

- Residential leases and PPAs qualify, too, but the leasing company, not the homeowner, claims the credit.

Note: Comparing solar loan vs lease vs PPA structures matters more now, since ownership alone determines who benefits.

Owned vs Leased Systems

Ownership determines who claims the federal solar tax credit, not who uses the electricity. A homeowner who purchased a $20,000 system in 2025 claimed the full $6,000 credit directly. A neighbor who signed a 25-year lease for an identical system never owned the equipment, so the leasing company claimed the corresponding Section 48E credit instead, sometimes passing partial savings through lower lease payments.

| Owned System | Leased System / PPA | |

| Who claims the credit | Homeowner | Leasing company |

| Legal basis | Section 25D (expired 2025) | Section 48E (active through 2027) |

| Credit received by the homeowner | Direct, dollar-for-dollar | Indirect, through lease pricing |

Commercial Bonus Credits

Commercial Section 48E projects can reach up to a 70% total credit value when combining all bonus add-ons onto the 30% base rate.

- The domestic content bonus adds 10 percentage points for qualifying projects that also meet prevailing wage and apprenticeship rules, or 2 points for those that don’t.

- The energy community bonus adds 10 percentage points for projects sited in coal closure areas, brownfields, or fossil-fuel employment zones.

- The low-income communities bonus adds 10 to 20 percentage points for facilities serving qualifying census tracts or Tribal land.

Note: Meeting prevailing wage and apprenticeship rules remains the gateway to the full 30% base; without it, the base falls to just 6%.

See the table below for a better understanding.

| Bonus Type | Increase | Key Requirement |

| Base rate | 6% → 30% | Prevailing wage + apprenticeship compliance |

| Domestic content | +2 to +10 points | U.S.-sourced steel, iron, components |

| Energy community | +10 points | Site in a qualifying energy community |

| Low-income / Tribal | +10 to +20 points | The facility serves a qualifying community |

State Incentives

State and utility programs add a second savings layer on top of any federal eligibility. The DSIRE database tracks active state and local incentives nationwide.

- New York’s NY-Sun initiative pairs with a state tax credit equal to 25% of system costs, capped at $5,000.

- California’s Self-Generation Incentive Program (SGIP) pays $150 to over $1,000 per kilowatt-hour for qualifying battery storage, depending on income tier.

Note: Many states also offer net metering, which credits solar owners for excess electricity sent back to the grid. These solar incentives by state programs remain unaffected by the federal Section 25D expiration.

How to Claim the Solar Tax Credit?

If you are a homeowner claiming a system operational by the late 2025 deadline, you will reconcile the credit during the 2026 tax filing season. The process requires filing a specific tax form alongside your standard individual return to calculate your final credit value and document any remaining balance to carry over into future years.

Note: Commercial entities follow a parallel path but use dedicated business credit forms to account for their multi-year carryback and carryforward options.

How to File Your Solar Return?

When you log into your tax software to file your return, follow these 3 steps:

- Complete IRS Form 5695 (Residential Clean Energy Credit) to calculate your total credit value or pull forward your unused rollover balance from the previous year.

- Carry that final calculated amount over to Schedule 3 (Form 1040), which handles nonrefundable credits.

- Apply the credit directly to line 19 of your main Form 1040 to cut your total tax liability dollar-for-dollar.

ITC vs Other Incentives: What’s the Difference?

The federal ITC differs from other solar incentives in structure and value.

- Net metering credits ongoing electricity use rather than upfront installation costs.

- State tax credits, like New York’s 25% program, pile on top of any remaining federal eligibility.

- MACRS depreciation lets commercial owners deduct equipment costs separately from the ITC. Additionally, properties updating their infrastructure often pair these projects with EV charger installation services to capture remaining localized alternative fuel vehicle refueling property incentives before their respective cutoff dates.

- The Production Tax Credit (PTC) offers commercial developers a per-kilowatt-hour alternative, currently valued near $0.026 per kWh, instead of an upfront percentage credit.

See the table for differences.

| Incentive | Type | Value | Applies To |

| Federal ITC (Section 48E) | Tax credit | 6%–70% of the cost | Commercial, leases, PPAs |

| Production Tax Credit (45Y) | Per-kWh credit | ~$0.026/kWh | Utility-scale alternative to ITC |

| MACRS + bonus depreciation | Tax deduction | Up to 100% of basis | Commercial systems only |

| State tax credit (e.g., NY) | Tax credit | Up to 25%, capped at $5,000 | State residents |

| Utility rebate (e.g., SGIP) | Upfront cash rebate | $150–$1,000+/kWh | Battery storage |

Suggestion: For business projects, compare solar tax incentives side by side before choosing a financing structure.

FAQ

Is the 30% solar tax credit going away in 2026?

Yes. Under the One Big Beautiful Bill (OBBBA), the federal residential Clean Energy Credit expired. The legislation ended the 30% credit for any clean energy expenses paid for after December 31, 2025. Homeowners who installed and placed solar panels in service on or after January 1, 2026, generally do not qualify for this federal residential tax credit.

Is there an income limit for the solar tax credit?

No. The federal solar tax credit never carried an income limit for individual or business filers. Eligibility depends only on ownership, system type, and placed-in-service timing, not adjusted gross income.

Does standalone battery storage qualify for the federal tax credit?

Yes, if owned outright and installed with at least 3 kilowatt-hours of capacity. IRS Form 5695 sets this minimum for the residential credit, while Section 48E covers larger commercial storage systems without that specific threshold.

What is the 20% rule in the solar world?

In the solar industry, the 20% rule is a design guideline ensuring your system generates about 80% of your home’s total energy consumption. The remaining 20% acts as a safety buffer to account for energy losses, unforeseen increases in demand, or battery capacity limits.

What are the limitations in claiming solar credits?

- You cannot claim the credit if your system is leased or through a Power Purchase Agreement (PPA) because you don’t actually own the panels.

- You can only claim the credit on the tax return for the exact year the system was fully installed, inspected, and actively producing power (Permission to Operate). This means you cannot claim it simply because you paid an invoice.

- Failing to keep proper records means an automatic rejection if the IRS audits your filing. You must retain an itemized invoice, proof of payment, and manufacturer certifications for the panels and inverters.

Do I get a cash refund for the excess credit?

No. Because this is a nonrefundable tax credit, you only benefit up to the amount of tax you owe.

Conclusion

The federal solar tax credit changed under the One Big Beautiful Bill Act of 2025. Section 25D no longer applies to residential systems placed in service after December 31, 2025. Section 48E remains active for commercial projects, leases, and PPAs through 2027, subject to new construction deadlines and FEOC rules.

Homeowners who installed systems before the deadline should file Form 5695 with their 2025 return and track any carry-forward balance. Commercial filers should confirm safe harbor status before July 4, 2026, and review bonus credit eligibility for domestic content and energy community adders. State programs, rebates, and net metering are still available regardless of federal eligibility.

If you want to determine your solar potential in this new regulatory landscape, whether for a third-party residential lease or a commercial property, contact the team at NEDES. We will review your current eligibility, compare optimized system designs, and provide free solar installation quotes before you commit.

Contact Solar Experts & Go Green With Confidence!