The End of the Traditional Solar Tax Credit In 2026 (And the Rise of Better Incentives)

Rumors spread fast in the renewable energy space. You might have heard whispers that the federal government is pulling the plug on solar subsidies, or that the golden era of government-funded solar installations has quietly passed. Let’s set the record straight right now. The federal solar tax credit is not dead. In fact, it remains locked in at a robust 30% through 2032.

But here is the catch that most solar installers will not tell you: treating that federal baseline as your only avenue for savings is a massive financial mistake.

Federal policy provides a great foundation, but it is a non-refundable credit. If you do not have the tax liability to absorb it, that 30% means very little to your immediate bank account. Furthermore, as the grid evolves and utility companies change their net metering rules, relying solely on a single federal solar tax credit leaves thousands of dollars on the table. There is a massive, often-ignored shadow market of local state credits, utility rebates, and performance-based payouts.

If you want to drop your installation costs to the absolute floor, you need to look beyond the federal baseline. This guide breaks down exactly how to pivot your strategy to leverage renewable energy tax incentives.

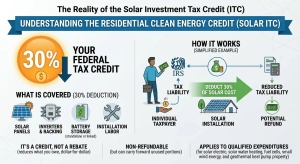

The Reality of the Solar Investment Tax Credit (ITC)

Before diving into the alternative programs, you need to understand exactly what the baseline federal offering does, and what it does not do. The solar investment tax credit (ITC), now officially referred to under the tax code as the Residential Clean Energy Credit, allows you to deduct a significant portion of your solar installation costs from your federal taxes.

Currently, the solar tax credit percentage sits at 30%. This covers the solar panels, inverters, racking equipment, battery storage systems (even standalone batteries), and the labor costs for installation.

The Non-Refundable Catch

Many property owners misunderstand how a tax credit for solar panels functions. It is not a cash rebate. The IRS does not mail you a check for 30% of your system cost upon installation. Instead, it reduces the federal income taxes you owe on a dollar-for-dollar basis. Know more about incentives and rebates for solar in our guide.

If you install a $20,000 solar system, your 30% credit equals $6,000. If your federal tax liability for the year is $4,000, the credit drops your tax bill to zero. The remaining $2,000 does not come back to you as a refund; it simply rolls over to the following tax year. For retirees or individuals with lower taxable incomes, the federal clean energy tax credit might take years to fully realize. This exact limitation is why hunting down local, cash-based solar rebate programs is critical.

State-Level Solar Energy Tax Credits: Your Second Line of Defense

While the federal government offers a blanket policy, individual states are fighting their own battles to meet clean energy mandates. To accelerate adoption, many states offer their own solar energy tax credit that stacks directly on top of the federal ITC.

Unlike the federal version, state incentives vary wildly. Some offer flat-rate cash rebates. Others offer a percentage-based state income tax reduction. By combining a state solar panel tax credit with the federal ITC, property owners in select regions can effectively wipe out 40% to 50% of their total gross installation costs.

Top State-Level Incentives in 2026

To give you an idea of what exists beyond the federal level, here is a breakdown of how some of the most aggressive state programs operate:

| State | Incentive Type | Maximum Benefit | Stacking Rules |

| New York | NY-Sun Megawatt Block & State Tax Credit | 25% of system cost (up to $5,000) | Stacks directly with Federal ITC. |

| Massachusetts | SMART Program & State Tax Credit | 15% of system cost (up to $1,000) | State tax credit applies; SMART pays out monthly cash based on generation. |

| South Carolina | State Solar Energy Tax Credit | 25% of system cost (up to $3,500/year) | Can carry forward unused credit for up to 10 years. |

| Illinois | Illinois Shines (SREC Program) | Varies based on system size (Cash payout) | Lump-sum cash payment for 15 years of expected solar generation. |

If you live in a state like New York or South Carolina, claiming your state’s solar power tax credit is just as important as filing for the federal ITC. Always consult a local tax professional to ensure you are maximizing both pools of money.

Solar Rebate Programs: Immediate Cash vs. Tax Delays

If you want immediate financial relief rather than waiting for tax season, solar rebate programs are your best target. These are typically offered directly by local utility companies or municipal governments. Because utility grids are aging and struggling to handle peak demand, power companies actually save money when you generate your own electricity. To encourage this, they offer upfront cash rebates.

Utility-Sponsored Rebates

Utility rebates usually function as a direct point-of-sale discount. If your utility company offers $0.50 per watt installed, a standard 8-kilowatt (8,000-watt) system would yield an instant $4,000 discount. The installer deducts this from your final invoice, meaning you do not have to wait until April to see the financial benefit.

Solar Renewable Energy Certificates (SRECs)

SRECs represent the hidden stock market of the solar industry. In states with Renewable Portfolio Standards (RPS), utility companies are legally required to generate a certain percentage of their power from renewable sources. If they fail to build their own solar farms, they must buy the “rights” to your clean energy.

For every megawatt-hour (MWh) of electricity your home generates, you earn one SREC. You can then sell these certificates on an open market to utility companies. Depending on your state, a single SREC can trade for anywhere from $10 to over $400. Over the 25-year lifespan of a solar system, SREC income can easily rival or surpass the value of the initial federal tax credit.

Navigating Residential vs. Commercial Solar Incentives

The pathways to maximizing solar ROI diverge significantly depending on whether the system is installed on a family home or a business. The residential solar tax credit focuses strictly on reducing personal income tax liability. However, the business sector unlocks entirely different financial mechanics.

If you are a business owner, the commercial solar tax credit includes aggressive depreciation rules that fundamentally change the math of solar investments.

The MACRS Depreciation Advantage

Businesses can leverage the Modified Accelerated Cost-Recovery System (MACRS). This is a specialized solar installation tax deduction that allows businesses to shorten solar panel payback period through depreciation deductions.

Under current tax law, businesses can depreciate 85% of the solar system’s value over a heavily accelerated five-year schedule. When you combine the 30% federal commercial ITC with the tax savings generated by MACRS depreciation, a business can often recoup 60% to 70% of the total solar system cost within the first five years of operation.

Comparing Residential and Commercial Benefits

| Feature | Residential Solar | Commercial Solar |

| Primary Federal Credit | 30% Residential Clean Energy Credit | 30% Section 48 Investment Tax Credit |

| Depreciation Eligibility | Not eligible | Eligible for MACRS (5-year accelerated) |

| Tax Equity Financing | Not applicable | Available (businesses can sell their tax credits to investors) |

| Direct Pay (Tax-Exempt) | Not eligible | Non-profits and local governments can receive the credit as a direct cash payment. |

As grid stability becomes a corporate priority, utilizing the commercial solar tax credit in tandem with MACRS turns solar from a simple environmental initiative into one of the most secure financial investments a company can make.

Mastering Solar Tax Credit Eligibility and Stacking Rules

Knowing that these incentives exist is only half the battle. Securing them requires navigating a labyrinth of red tape. Strict solar tax credit eligibility guidelines dictate who gets paid and who gets left behind.

To ensure you successfully claim the vast array of solar energy incentives USA markets have to offer, you must understand the rules of “stacking.” Stacking refers to claiming multiple incentives on the exact same solar installation. While perfectly legal, the order in which you claim them matters immensely.

The Golden Rule of System Ownership

The most critical eligibility rule across almost all programs is ownership. If you lease your solar panels or sign a Power Purchase Agreement (PPA), you do not own the system. The third-party solar company owns the equipment on your roof. Therefore, the solar company claims the federal ITC, they claim the state tax credits, and they harvest your SRECs.

To claim a tax credit for solar panels, you must purchase the system either with cash or through a solar loan. As long as your name is on the title of the equipment, the incentives belong to you.

How to Calculate Stacked Incentives Safely

When you combine a state rebate with a federal tax credit, the IRS requires you to calculate the federal credit based on the net cost of the system, not the gross cost, if the state incentive is considered a utility rebate.

Here is how the math works in reality:

- Gross System Cost: $25,000

- Minus Utility Cash Rebate ($3,000): Your new taxable basis is $22,000.

- Calculate Federal ITC (30% of $22,000): $6,600.

- Calculate State Income Tax Credit (e.g., 10% of $22,000): $2,200.

- Final Net Cost: $13,200.

By understanding how a utility rebate lowers the baseline for your tax credits, you avoid costly IRS audits while still slashing the final price tag of your system by nearly 50%.

The landscape of renewable energy funding is shifting. While the federal baseline remains secure for now, the smart money is heavily focused on the local level. Grid operators are desperate for decentralized power, and state governments are willing to pay top dollar to anyone willing to generate it.

The Battery Storage Loophole

Historically, energy storage was an administrative gray area. If you wanted a tax break on a home battery, it strictly had to be charged entirely by your solar panels. That restriction is gone. Changes to the solar investment tax credit (ITC) have blown the doors wide open for battery adoption.

Because grid instability and blackouts are at an all-time high, the government is aggressively incentivizing energy storage. You can now apply the 30% clean energy tax credit to standalone battery systems with a capacity of at least 3 kilowatt-hours (kWh). You no longer even need to install solar panels to claim this specific incentive.

Why does this matter? If you live in an area with aggressive Time-of-Use (TOU) utility rates, you can install a standalone battery, charge it from the grid overnight when power is dirt-cheap, and discharge it to power your home during expensive evening peak hours. You slash your utility bill, and the federal government still subsidizes 30% of the equipment and installation costs. Of course, pairing it with a full solar array is the ultimate goal, but utilizing this storage-specific solar power tax credit is a phenomenal standalone strategy.

The “Free Roof” Trap: What the Solar Panel Tax Credit Actually Covers

We need to address a widespread industry scam. Dodgy salespeople door-knocking in your neighborhood will often pitch an irresistible deal:

“If your roof is old, we will replace the whole thing and bundle it into your solar loan. You can claim the 30% tax credit on the entire project!”

This is categorically false. It is tax fraud, and the IRS is aggressively auditing homeowners who attempt it.

The tax credit for solar panels strictly applies to the equipment that directly generates or stores electricity. Traditional roofing materials (even if they must be replaced to support the weight of the panel) do not qualify. Understanding exactly what falls under the umbrella of solar tax credit eligibility will save you from devastating IRS penalties.

Authorized vs. Unauthorized Expenses

Here is a clear breakdown of exactly what the IRS allows you to claim when calculating your solar tax credit percentage:

| Expense Category | Eligible for 30% Tax Credit? | IRS Rationale |

| Solar Panels & Inverters | Yes | Core generation equipment. |

| Labor & Permitting | Yes | Essential installation costs, including developer fees and inspection costs. |

| Battery Storage (3kWh+) | Yes | Authorized energy storage hardware. |

| Sales Tax | Yes | Treated as part of the total system cost. |

| Traditional Shingles/Roofing | No | Serves a structural function, not an energy-generating function. |

| Structural Reinforcements | No | Rebuilding trusses or decking to support panels does not qualify. |

| Tree Removal | No | Clearing shade from your property is considered standard landscaping. |

The One Exception: Solar roofing tiles. If you install integrated solar shingles (like the Tesla Solar Roof or GAF Energy Timberline Solar), the shingles themselves serve as both the roof and the energy generator. In this highly specific scenario, a larger portion of the roofing project qualifies for the residential solar tax credit.

Paperwork Execution: How to Actually Claim the Federal Solar Tax Credit

Accruing renewable energy tax incentives on paper means nothing if your CPA fumbles the execution. Claiming the baseline federal credit requires precision during tax season.

To secure your federal solar energy tax credit, you or your accountant must file IRS Form 5695 (Residential Energy Credits) alongside your standard Form 1040.

Here is the strategic workflow to ensure nothing gets missed:

- Retain Your Final Invoice: Do not rely on your initial sales proposal. The IRS requires the final, paid-in-full invoice reflecting the completed installation.

- Verify the “Placed in Service” Date: You cannot claim the credit simply because you bought the panels. The system must be fully installed, inspected, and granted “Permission to Operate” (PTO) by your utility company. If you buy panels in December 2026 but PTO occurs in January 2027, the credit applies to your 2027 tax year.

- Calculate Carryforward: If your 30% credit amounts to $9,000, but you only owe $5,000 in federal taxes, input the $5,000 limit on your current year’s return. Form 5695 includes specific lines to calculate your $4,000 “carryforward” amount, which will roll into the next year. Keep meticulous records of this rollover.

Book Your Free Consultation Now

The Commercial Leasing Loophole: A Tax Strategy for Non-Profits

We touched on the commercial solar tax credit earlier, but there is a specific mechanism that unlocks solar for entities that traditionally could not afford it: the tax equity market.

Historically, non-profits, churches, and public schools could not benefit from a solar installation tax deduction or credit because they do not pay federal taxes. A non-refundable credit is useless to a tax-exempt organization.

However, savvy solar developers use Third-Party Ownership (TPO) models to bypass this. A commercial developer will install the solar system on the church’s roof at no upfront cost. Because the developer is a for-profit business, they legally claim the massive commercial solar tax credit and MACRS depreciation. They then pass a portion of those immense tax savings down to the non-profit by selling them the solar electricity at a heavily discounted rate.

While the Inflation Reduction Act did introduce a “Direct Pay” option allowing some tax-exempt entities to receive the ITC as cash, the administrative burden is heavy. Leveraging a developer’s ability to claim the credit often results in faster, cheaper, and lower-risk solar deployments for community organizations.

Time is Running Out on Local Funds

Here is the harsh reality of solar energy incentives USA. The federal government has deep pockets; local governments do not.

While the baseline federal federal solar tax credit is locked at 30% until 2032, state and utility solar rebate programs operate on fixed, limited budgets. They utilize “step-down” block programs. This means the incentive payout drops as more megawatt capacity is installed in the state.

For example, a state might offer a $1,000 rebate to the first 5,000 homeowners who go solar. Once that quota is hit, the rebate drops to $750 for the next block, then $500, until the budget is entirely depleted.

If you spend months debating whether to pull the trigger on a solar installation, your federal benefits will remain perfectly safe. But your local utility rebate? Your state income tax reduction? Your SREC payout rates? Those are evaporating by the minute.

The Bottom Line

Stop viewing the federal 30% tax credit as the ultimate goal of your solar journey. It is merely a safety net. The true financial victors in the renewable energy space are the property owners who aggressively hunt down utility cash rebates, trade their SRECs on the open market, and stack every available state tax reduction on top of the federal baseline.

The money is sitting there, already allocated by local governments to upgrade the grid. If you do not claim those funds to put panels on your roof, your neighbor will claim them for theirs. Optimize your tax strategy, find a reputable local installer, and start stacking your incentives before the local budgets run dry.

Frequently Asked Questions

Is the federal solar tax credit still available for homeowners in 2026?

The direct-purchase residential credit (25D) technically expired for new systems in 2026. However, homeowners can still capture federal benefits through solar leases or PPAs, where providers claim the commercial credit and pass savings to you.

Can I still get a tax credit for solar battery storage?

Yes. Standalone battery storage with a capacity of 3kWh or more remains eligible for a 30% federal tax credit. This is a vital loophole for those looking to secure their energy independence despite solar-specific shifts.

What happens if my state doesn’t offer a solar tax credit?

Even without a state-level credit, you can achieve massive savings through utility rebates, SREC sales, and property tax exemptions. Many utilities pay upfront cash incentives that significantly lower your net installation costs immediately.

Do I need to own the panels to get the tax credit?

To claim the federal credit directly on your tax return, you must own the system. If you choose a lease, the installation company receives the credit, typically resulting in lower monthly payments for the homeowner.

How does the commercial solar tax credit differ in 2026?

Unlike the residential side, the commercial solar tax credit remains robust. Businesses can claim the 30% credit and utilize accelerated depreciation (MACRS), often recovering more than half of the system cost within five years.

What is the Safe Harbor rule for solar projects?

For larger or commercial projects, the “Safe Harbor” rule allows you to lock in the 30% credit rate if you began physical construction or spent 5% of the project cost before specific 2026 deadlines.